Sweat The Business Stuff: What Type of Business Are You Running Anyway?

/

About halfway through my TV producing career, I decided that I had gained enough experience and made enough connections to strike out on my own. When I told my friends and colleagues about this plan, they all asked the same question:

“Are you going to incorporate?”

My answer was always “yes.” I knew that incorporating was important, though at the time I didn’t really know WHY it was important, beyond some vague notion that it had to do with taxes. Eight years - and an expensive legal education - later, I can now tell you.

Forming a business entity legitimizes you and your work in the eyes of your peers, clients, and industry. You’re not just a person working alone in a poorly ventilated basement (although you may actually be that); you're a capital-B Business with real prospects and a real product or service. In other words, you look credible.

That credibility comes from the structure a business entity takes, as well as its related protections and benefits. It lets the other party feel assured that if something happens to the deal, there's a legal framework there to pick up the slack. So choosing the right corporate entity is paramount because each one functions a bit differently from the others.

There are four main business types - the Sole Proprietorship, the Corporation, the LLC, and the Partnership. I'm going to give you a brief rundown of the pros and cons of each, so bear with me... this is going to get long and boring. Sorry.

The Sole Proprietorship

"Knock knock."

"Who's there?"

"Just you, buddy."

A sole proprietorship is the simplest kind of business because it's literally just you. There's no legal or corporate structure to be had, which makes it a favorite of artists and designers who want to invest the least amount of effort into the business side of things.

Formation of the entity: Maybe the biggest advantage of the sole proprietorship is that once you decide to go into business for yourself, there's nothing further you have to do to set up the business - beyond getting a website, domain name, and building a client network. No contracts, formation papers, operating agreements, or articles of incorporation are necessary.

Taxation: Because the business entity is just you, you will be taxed as you are now, on your personal income. The business is not taxed separately.

Limited liability: This is where things get tricky. The upshot to a sole proprietorship is that because it's just you, there's very little in the form of paperwork. The downside is that because it's just you, there no real legal entity to speak of that protects you from lawsuits. This means that if the business is sued, you are personally liable, and the opposing party can come after your personal assets - bank accounts, your home, your car, etc. Many professionals will often choose to acquire some form of liability insurance just to hedge against this kind of thing.

Why choose it? Because you’re a single-person business who doesn’t want partners, employees, an office, or much in the way of business structure. If it’s just you and you want to keep it that way, a sole proprietorship is the most appealing option. The business lives and dies with you, which some find appealing. My law practice, for example, is a sole proprietorship because I don’t want the muss and fuss that comes with owning a business. Lean and mean is my game, which makes my overhead low and keeps the day-to-day business operations stuff that I hate to a minimum.

The Corporation

You know what a corporation is. They run the world and rule your bank account. They have more say about your daily life than you probably do.

Formation of the entity: To form a corporation, you generally need to A) file incorporation papers with the state and IRS (to get an Employee Identification Number), B) create and file an operating agreement between the owners and directors of the business dictating the responsibilities and duties of the members, and C) create bylaws that govern the way the business operates. Forming a corporation is not for the faint of heart or the part-time business owner. It’s a serious investment in time and capital and it operates under the impression that the business will, for all intents and purposes, live forever.

Taxation: When you form a corporation, you’ll not only pay traditional income tax on whatever personal income you earn working for the business, but the corporation will pay taxes on its earnings and profit as well. In the business and legal world, this carries the misnomer “double taxation” which isn’t indicative of what’s really happening, but it sure sounds bad, right? This is one reason why so many corporations try to minimize their tax liability through loopholes and other shady practices (also, to maximize profits). It’s also why so many corporations form in Delaware - because of that state’s permissive and business-friendly tax laws.

Limited liability: This is the main benefit to forming a corporation. The corporate structure limits liability to corporate assets, which means that if the company is sued during the course of business, the plaintiff can only go after business assets, leaving your personal assets safe. Every so often, cases arise where plaintiffs can “pierce the corporate veil” and go after your personal assets, but it’s usually in cases of fraud or other wrongdoing where the corporate entity is used as a shell to cover up bad acts.

Why choose it? What do they say? Go big or go home? That’s why you start a corporation. You want to go big. You want the business to live forever. There’s a lot of money to be made and you need all sorts of businessy stuff to make that happen - a board of directors, offices, corporate structure, profit, the whole nine yards. When you absolutely positively want to master your industry, accept no substitutes.

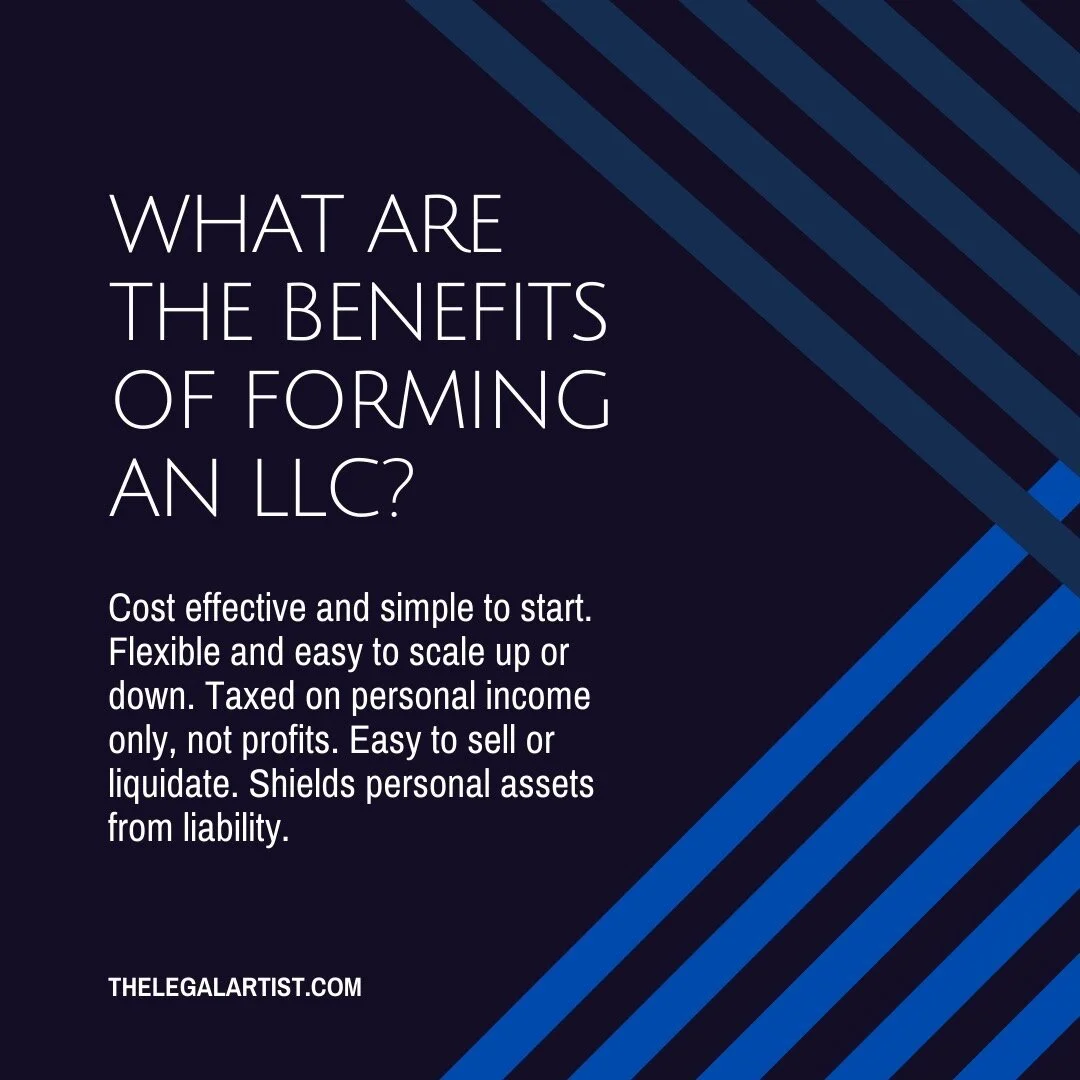

Limited Liability Corporation

How do you get the liability benefits of a corporation but the single taxation of the sole proprietorship without starting either or both? You form an LLC! This is by far the most common and preferably method of forming a company that I’ve ever seen and the one that appeals most to small business owners and artrepreneurs alike. It’s flexible and combines the benefits of both types of entities without most of the drawbacks.

Formation of the entity: Like a corporation, you need to file your articles of incorporation with the state and IRS. Some states may require you to file an operating agreement as well, even if you’re a single-person LLC. As a rule, it’s a pretty good idea to have an operating agreement on hand anyway because that document will outline what your duties and obligations are.

Taxation: This is why people like LLCs. Unlike traditional corporations, LLCs are “pass through” entities, meaning that you don’t have to pay tax on your corporate profits, just on the personal income you make.

Limited liability: This is the other reason people like LLCs; you have the same limited liability benefits bestowed on corporations.

Why choose it? Let’s be honest, you’re going to start an LLC. I don’t know why I even wrote about the other business types because this is likely where it begins and ends for you. You’re going to start an LLC because you want the flexibility and you don’t want to pay a ton in taxes to the state. Your business (like most in America) is probably a small one and it’s unclear how big it’s going to get, or even how big you want it to get. That’s why the LLC was created to begin with: so people could start small businesses without getting taxed into oblivion. Not everyone wants to be the next Facebook, Microsoft, or IBM. Sometimes you just want to start a neighborhood dry-cleaning business.

Partnership

In law school, a professor once told our class that if we ever counseled a client to form a partnership, that would be tantamount to legal malpractice. I’m pretty sure he was joking, but he has a point. Unless you’re a lawyer, doctor, or accountant, a partnership is literally the worst business entity you can possibly form. Why? Find out below.

Formation of the entity: Like a sole proprietorship, you are not obligated to register your partnership with the state or IRS. You are, however, obligated to create a partnership agreement between yourself and your other partners outlining your duties and obligations to each other. This is a crucial document and if you enter into a partnership (already off to a bad start) without an agreement, well what can I say? You’re a dummy that deserves whatever horrible outcome happens.

Taxation: Ah the single benefit to the partnership. Instead of the partnership being taxed as a corporate entity, or you being taxed on your income, you pay taxes (individually) on your profits. This means you’re taxed at the lower capital gains rate of 20% than the regular income tax rate.

Limited liability: This is why partnerships suck. There is no limitation on liability. You are personally liable not only for your own actions, but the transgressions and bad acts of your partners as well. In fact, you can be liable for the bad acts of former and dead partners too! There’s a reason you only see professionals like doctors, lawyers, and accountants form partnerships… because members of these industries have malpractice insurance that help protect them and cover the losses from lawsuits stemming from the bad acts of a partner.

Why choose it? Don’t. Just don’t do it. Seriously.

Bored yet? Look I know this stuff isn’t going to set your world afire (and believe me, I’ve left out a lot of detail here just to keep the information dump manageable), but many of the artists, designers, and filmmakers who come to me for legal representation are looking to start small businesses and don’t know where to start. Knowing your options is a good way to at least start figuring out how to move forward.